Client interview | Outsourcing service for financial results disclosure

Riso Kyoiku Co., Ltd.

Transitioning from a reactive approach to assertive disclosure

Developing young talents and elevating accounting departments through outsourcing

The financial reporting process has been subject to mounting complexity as a result of successive amendments to rules including those for contending with new disclosure systems. With this compounded by increasingly chronic labor shortages when it comes to practitioners in the front lines, it is no exaggeration to say that operational workloads are escalating. Under these circumstances, a growing number of companies have begun adeptly turning to outsourcing services. Riso Kyoiku Co., Ltd. is one such company. They have adopted and integrated the outsourcing service for financial results disclosure provided by PRONEXUS into its operations. Riso Kyoiku particularly expects more sophisticated operational procedures. We interviewed Mr. Yusuke Shimizu and Mr. Ryonosuke Oyamada, who respectively serve as manager and assistant manager in Riso Kyoiku’s Accounting Section, Corporate Planning and Administration Department. We asked them about key solutions that have been identified through our outsourcing service for financial results disclosure.

Company profile

- Company name

-

Riso Kyoiku Co., Ltd.

- Listing

-

Prime Market

- Fiscal year-end

-

February

- Description of business

-

Private tutoring schools and education services

- Number of employees (consolidated)

-

1,119 (as of February 29, 2024)

- Number of employees in charge of the financial reporting process

-

5 (as of January 31, 2025)

- Number of consolidated subsidiaries

-

7 (as of January 31, 2025)

- Audit firm

-

Ernst & Young ShinNihon LLC

Effective improvement achieved through visualization of the financial reporting process

You started using the outsourcing service for financial results disclosure beginning with the fiscal year ended February 28, 2022. What sorts of challenges were you facing at that time? Please also explain the factors underpinning your decision to adopt the service.

Mr. Shimizu:

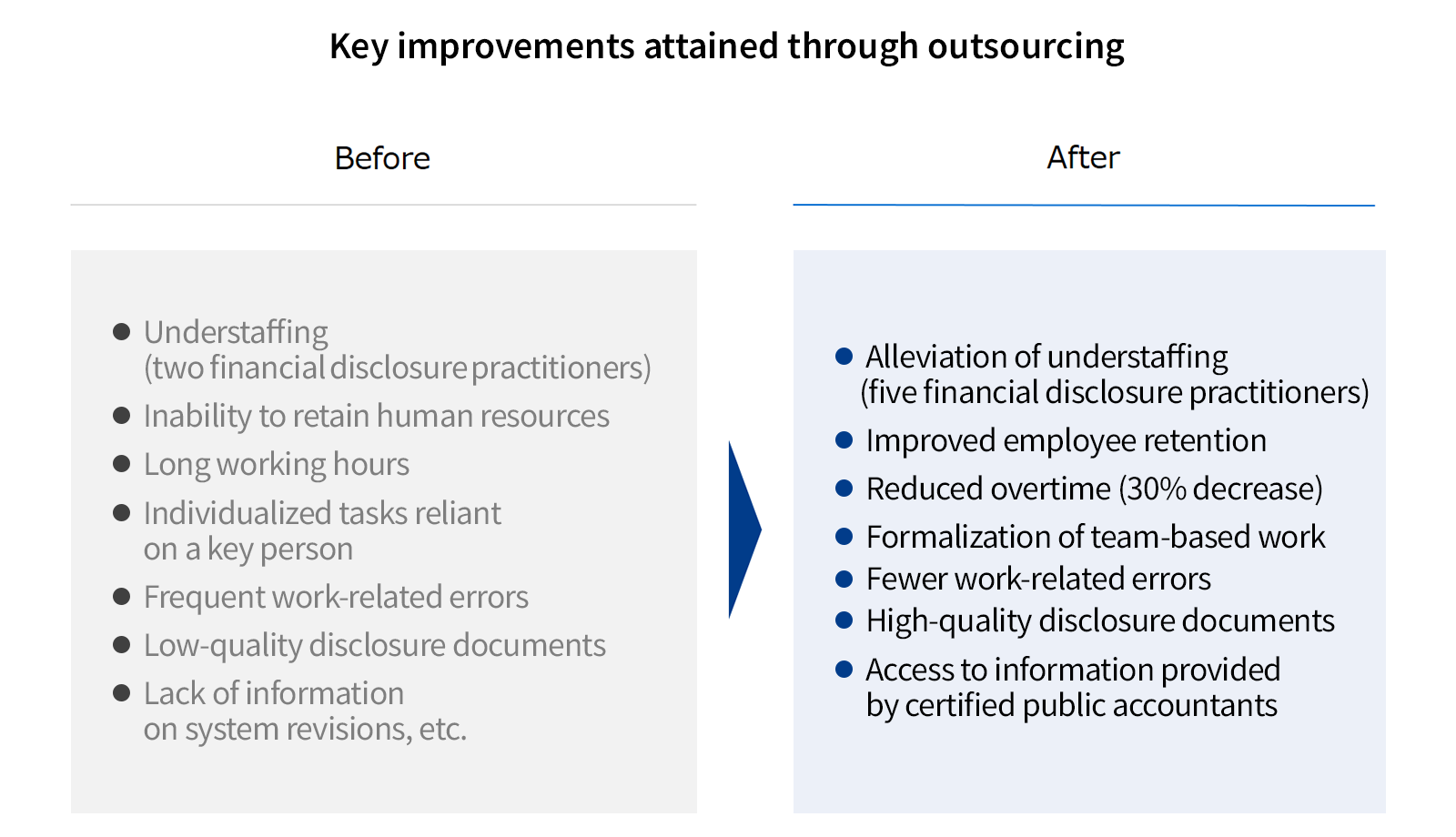

Only two employees, including myself, were engaged in the financial reporting process at the time, which inevitably resulted in frequent overtime.

Consequently, we were forced to submit substandard disclosure documents to our audit firm, resulting in the need for repeated revisions to address identified concerns.

We decided to explore the option of turning to an outsourcing service in seeking to address that situation.

This is because we needed to enhance the entire financial reporting process, above and beyond reducing operational workloads merely through outsourcing of data entry.

Given the limited operational experience of our team members at the time, we deemed sophisticated external support as essential for achieving fundamental improvement in our operational processes.

With numerous outsourcing services available, what considerations went into your decision to adopt our service?

Mr. Shimizu: Many companies offer outsourcing services. In exploring our options, we sought materials on various services and attended briefing sessions. However, we already had an ongoing business relationship with PRONEXUS, which culminated in our decision to implement the service on a three-month trial basis starting from the second quarter of the fiscal year ended February 28, 2022.

――What did you learn as a result of the trial implementation?

Mr. Shimizu:

We determined that the service had potential to fundamentally improve our operational processes.

An example of this is the handling of fundamental materials used by accounting in order to prepare disclosure documents.

基礎資料を基にPRONEXUS While this involves entering data into the PRONEXUS WORKS platform based on fundamental materials, the outsourcing service for financial results disclosure also entailed working with in-house source materials that were out of order. This involved listing and numbering such materials in Excel and systematically filing them in a shared folder.

This was a proposal for improvement that looked beyond data entry to also consider operational simplicity with the future in mind.

With only two team members previously, we lacked the capacity to organize these fundamental materials.

We felt there was no need to reorganize and list such materials at the time because we had a sense of where each document was located based on experience.

However, when document management is reliant on a key person, it becomes confusing and inefficient for new employees.

Given that we deemed the service to be highly beneficial in terms of developing a framework that anyone can understand, we decided to fully adopt the service in seeking ongoing improvement.

Transitioning from operations reliant on a key person to an organizational teamwork approach

In what other ways do you think full implementation of the service was effective?

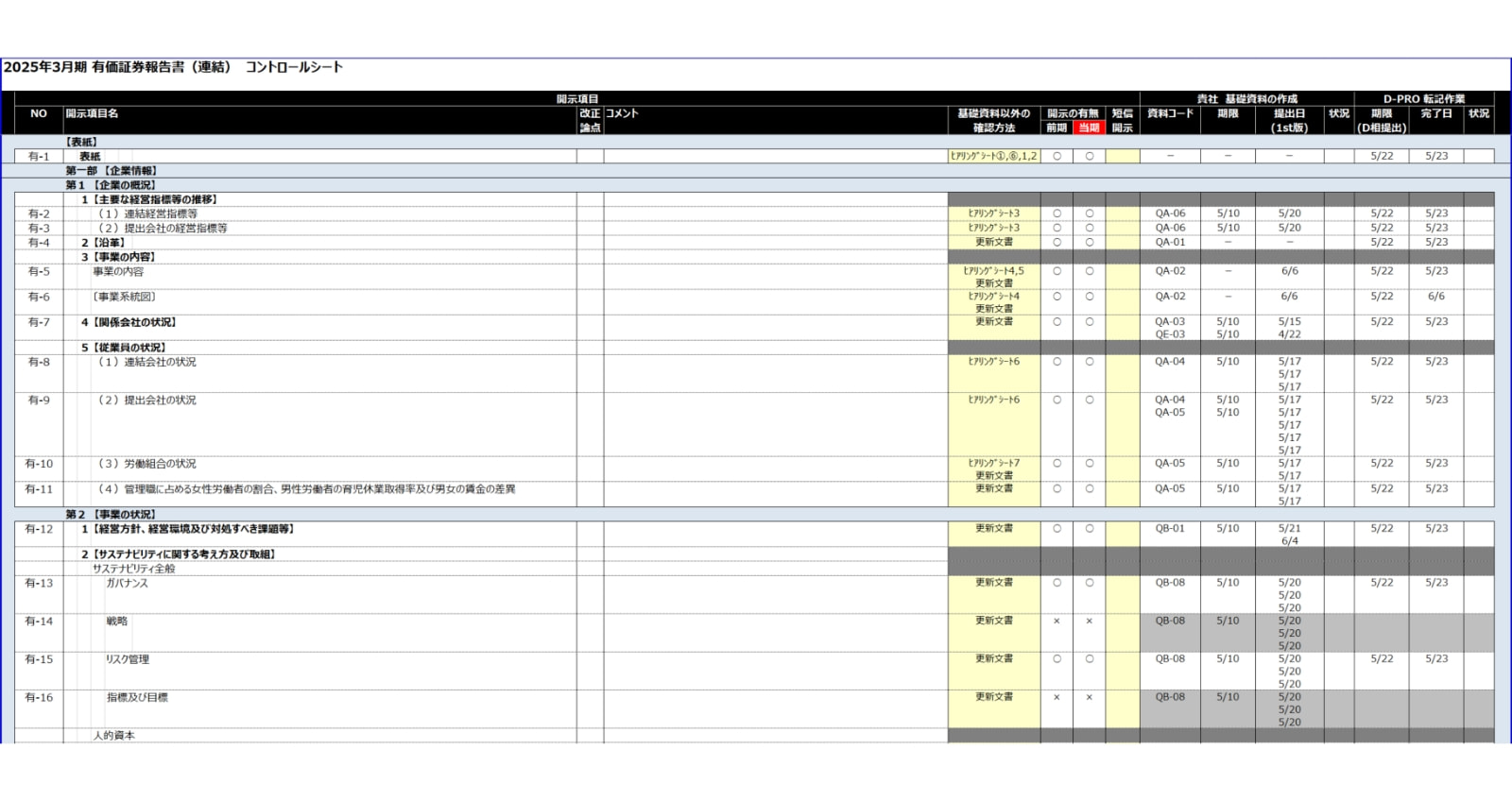

Mr. Oyamada:We are now able to visualize respective operations through use of a control sheet, which serves as a blueprint in mapping fundamental materials to specific disclosure document sections.

Typical control sheet

Mr. Oyamada: It has become easier for us to allocate tasks to team members because we now have a clear idea of who handles what, by when, and to what extent. Whereas it is possible to assign tasks immediately with little effort, ensuring that operations are visually mapped out is essential. This is important when it comes to newly hired employees engaged in the financial reporting process for the first time because a lack of understanding regarding their current job assignments impedes the learning process and causes anxiety.

We have been told that the service has also contributed to employee retention. In the current hiring market, many companies continue to face difficulties in recruitment given that professionals with experience in the financial reporting process are often drawn to startups and other enterprises offering attractive employment conditions. Amidst this situation, Riso Kyoiku increased its workforce of professionals engaged in the financial reporting process to a team of five employees from two employees initially. How did you manage to elevate your organizational capabilities under these circumstances?

Mr. Shimizu: Of course, we also struggle with attracting experienced professionals. That said, we need to develop talent in-house given such difficulties we face in recruitment. We have accordingly opted to develop talent in-house because we have managed to attract many young talents who lack experience in financial disclosure but fortunately have accounting experience and are eager to learn. As mentioned earlier, the outsourcing service has made it easier for us to assign duties because use of its control sheets makes it possible to immediately identify who is responsible for what, and to what extent. Meanwhile, creation of job rotations aligned with proficiency of our key personnel helps us develop talent capable of handling overlapping tasks. This ensures that knowledge transfer and practical training are accomplished simultaneously. The outsourcing service improves our financial reporting process, while also offering the significant advantage of enabling our young talents to fulfill their aspirations in allowing them to systematically amass experience from the ground up.

Harnessing the insights of highly-skilled professionals

What kind of advice have you received from the CPAs of DISCLOSURE PRO who support your financial reporting process?

Mr. Shimizu: We reflect on our financial reporting practices with CPAs following each accounting period. Advice we have received on fine-tuning our fundamental materials has been very useful. The CPAs identify areas for improvement of our fundamental materials each time we meet, which enables us to approach the next financial results cycle with better fundamental materials. We have also consolidated multiple fundamental materials into a single document, which streamlined our operations. Putting CPA advice directly into practice has resulted in tangible improvement, making the process easier with each subsequent cycle. Meanwhile, reducing man-hours by eliminating redundant tasks has enabled us to complete our operations in less time. Being able to rely on advice from the CPAs has also afforded us considerable peace of mind.

Mr. Oyamada: Another appealing aspect of the CPA support is the advice we receive on key implementation issues arising from amendments, particularly those related to accounting standards and system revisions. While it is important for everybody to stay informed, we also need to efficiently elevate understanding of the entire team. The CPAs at DISCLOSURE PRO are helpful in that they provide us with concise explanations of key points, while also considering how these changes specifically impact our company. A recent example of this that comes to mind has to do with our disclosure of sustainability information in our securities report, initiated in April 2023. I think we would have missed our deadline if we had taken it upon ourselves to research the relevant information upon its release by the Financial Services Agency in attempting to determine our internal response. Because we promptly received advice specifically tailored to our situation, we were able to anticipate a course of action early on.

Transitioning from a reactive approach to assertive disclosure

― How are you allocating time you have saved now that you have reduced your data entry workload and achieved more effective disclosure practices?

Mr. Oyamada: The service enabled us to cut overtime by about 30% in one of the initial months of its implementation, which made us aware of the service’s tangible results. We have since increased our headcount and achieved a significant reduction in concerns identified by our audit firm. The extra time gained has enabled us to focus on preparing internal materials while devoting more time to management reporting.

Please tell us about new objectives and challenges you expect to encounter going forward.

Mr. Shimizu: In terms of the financial reporting process, our ultimate aim is to ensure that we prepare lucid materials tailored to investors who hold our shares. We are now able to efficiently handle reporting in alignment with certain standards by adhering to previous formats, but our disclosure documents are quite simple, for better or worse. I think it will be possible for us to create more visually accessible materials through the inclusion of charts and tables. If we manage to allocate more time for internal discussions and dedicate effort to refining our fundamental materials, we should be able to create documents that stimulate investor engagement. We hope to eventually achieve a standard of disclosure worthy of inclusion in the Financial Services Agency’s compilation of best practices. Such recognition would also conceivably translate to greater appeal externally. We envision a gradual shift to more assertive disclosure through these efforts, from our reactive approach thus far.

- The preceding content has been prepared based on various sources of information available as of the date on which this document was released.